Skift Take

Sell them off, split them up, and move them around, sure, but it won't solve many of the underlying problems that Bloomin' and its competitors and contemporaries are having: Customers just aren't as interested in what they have to sell these days.

— Jason Clampet

Bloomin’ Brands Inc. could soon join a boomin’ M&A trend.

Activist investor Jana Partners disclosed a stake in the Outback Steakhouse operator on Monday and said it may push for a sale or operational changes. A 30 percent premium to Bloomin’ Brands unaffected stock price indicates a takeover value in the range of $3.3 billion, including $1.1 billion in net debt. Analysts have speculated Jana’s true aim is a breakup: CL King’s Michael Gallo estimates the Bonefish and Carrabba’s chains could command $1 billion combined. Bloomberg Intelligence’s Michael Halen says Fleming’s Prime Steakhouse & Wine Bar is a weird fit and could fetch more than $350 million on its own.

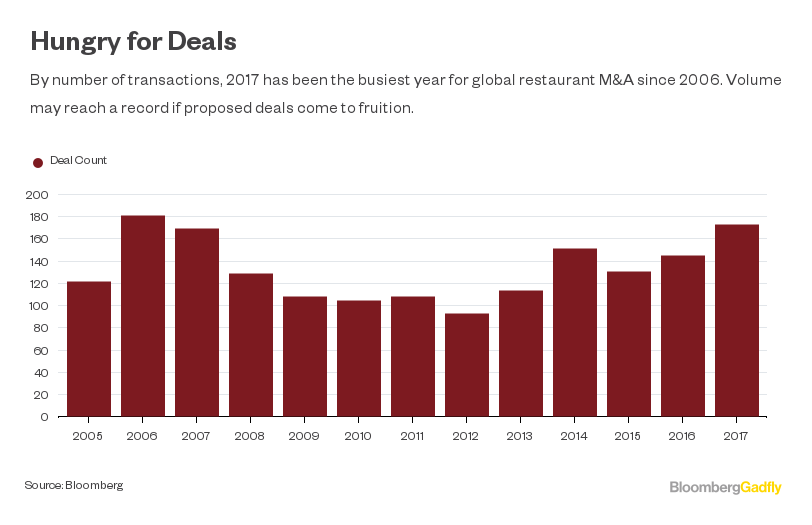

Whether Bloomin’ Brands is sold in pieces or as a whole, any transaction would send an already-rising tally of restaurant M&A even higher. There have been 173 eatery takeovers announced globally so far this year, the highest count since 2006, according to data compiled by Bloomberg. Should prospective targets such as Bloomin’ Brands, Buffalo Wild Wings Inc. and Jack in the Box Inc.’s Qdoba Mexican restaurant actually be acquired, transaction volume for the industry could hit a record.

What’s driving all this activity? Restaurant operators are increasingly turning to consolidation to grow their revenue as they start to realize the pitfalls of over-expansion. America only needs so many Olive Gardens, after all. And that’s especially true when eating in is becoming cheaper and easier, thanks to grocery store price wars and meal-delivery services like Blue Apron Holdings Inc. Restaurants are fighting with each other and themselves for a shrinking pile of dollars. With debt still cheap, taking out your competitor is a prudent bet.

And then there are the private equity buyers, which have accounted for nearly a fifth of this year’s restaurant deal count. Some may have the same consolidation goals in mind; Golden Gate Capital, for example, bought Bob Evans Farms Inc.’s restaurant business this year, adding to investments in Red Lobster and California Pizza Kitchen. Buffalo Wild Wings suitor Roark Capital Group has also invested in Arby’s, Culver’s and Jimmy John’s.

Other buyout firms are looking to accelerate the budding growth of upstart chains that cater to customers’ increasingly healthy tastes and interest in fast-casual dining. Just this month, an arm of TPG agreed to take a majority stake in sandwich-and-salad chain Mendocino Farms, and a Beekman Group fund invested in “better breakfast” brand Another Broken Egg of America.

If private equity firms are looking to put money to work in the consumer space, restaurants are an easier sell to their investors than retailers right now, given the general sense of apocalypse in the latter sector, says Bloomberg Intelligence’s Halen. There’s less risk of Amazon.com Inc.-like usurpation. People have to eat, and even with the advancements in food delivery, there’s still something to be said for the experience of dining out.

All of these trends should continue into 2018, meaning the motivations for M&A will stay strong. Who does the buying next year, however, will be somewhat dependent on the final form of Republicans’ tax plan, as Bloomberg Intelligence notes.

Private equity firms would be hamstrung by a proposed cap on interest deductibility. Only takeovers that require lower leverage would still be financially attractive. Whether or not the average American is actually going to get a tax cut is unclear, but the idea at least is to increase disposable income, something that should help restaurant traffic. Betting on tax reform actually happening is a risky game, though. And barring any tax-driven traffic increase, restaurants that have largely sat out this M&A wave may feel pressured to get involved.

Cheesecake Factory Inc., for example, has talked about eventually growing to 300 U.S. locations. It has 196 company-owned namesake restaurants in the country currently. Why not instead buy some hot emerging brand to grow market share, asks Halen? He’s got a point. Here’s looking at you, 2018 restaurant M&A.

©2017 Bloomberg L.P.

This article was written by Brooke Sutherland from Bloomberg and was legally licensed through the NewsCred publisher network. Please direct all licensing questions to [email protected].

![]()