Skift Take

Keeping all stakeholders happy may require Uber Eats to improve current relationships with eateries via marketing incentives or lower commission fees, perhaps at the expense of its own bottomline. Investors will surely not like that very much.

— Danni Santana

London restaurateurs call them “helmet heads”: the food delivery couriers who congregate in eatery doorways as they await an order, their moped or bicycle perched on the adjacent curb.

In the U.S. they work for Uber Technologies Inc., GrubHub or Postmates. The U.K. has Deliveroo as well as Uber Eats; Germany has Foodora. Each firm increases tension in the restaurant industry, because the rise of app-based meal ordering is exerting substantial pressure on venues’ bottom line.

This creates a substantial challenge as it prepares an initial public offering: Uber may have to pare its take from restaurants while assuring would-be stock investors it has a path to profitability. That doesn’t augur well for its own long-term prospects.

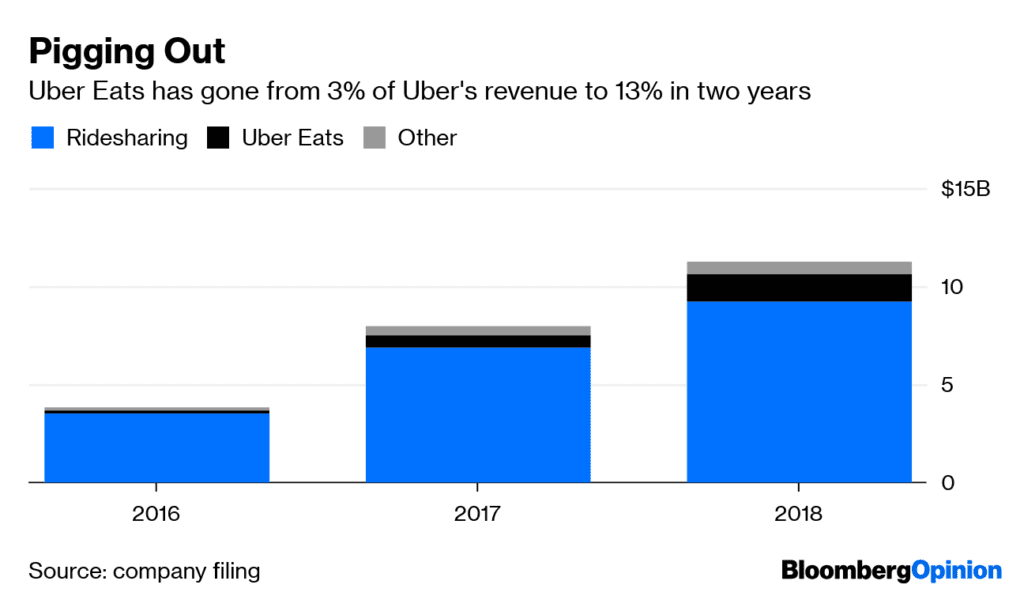

The growth of Uber Eats is a story that the San Francisco-based firm is eager to recount. Chief Executive Officer Dara Khosrowshahi sees his food business as proof that his firm will ultimately be so much more than just a ridehailing company, but the last mile delivery service for any number of products.

So far, the performance has been overwhelmingly positive. Uber Eats revenue jumped almost threefold to $1.5 billion last year, faster than the company-wide 42 percent growth rate.

But there’s a lot for restaurants not to like about the arrangement.

Sure, third-party delivery services such as Uber Eats and Deliveroo are useful for driving growth. That’s helpful if you have outside investors. But they can be very bad for profit.

For one, people ordering food are less likely to buy drinks, alcoholic or otherwise, than if they eat in a restaurant. Because it takes less time to open and pour a bottle than it does to cook almost any dish, beverages on the whole require lower labor costs and offer higher margins. With each beverage-less order, restaurants sacrifice a lucrative piece of their business.

Then there are the commissions on the delivery. These can reach 35 percent of the order value, according to merger consultant Dealroom.co.

Proprietors are also concerned about the potential for damage to their reputation, according to Bob Goldin, co-founder of food industry strategy consultant Pentallect Inc. The moment they hand an order over to a courier, they lose all control over the condition in which the food arrives at its destination. Yet it’s the restaurant that’s usually suffers any blowback.

There’s also something amiss with Uber’s sales pitch. The service is supposed to help kitchens work at full capacity in fallow periods. But peak order times are also usually peak periods of demand to eat onsite. The logical solution would be for a restaurant to reject orders when it doesn’t have the capacity. But if it does so, it risks getting pushed down the rankings in search results — Deliveroo and rivals have similar policies — making it less likely to get new business.

If the food industry starts deciding that the growth prospects aren’t enough to offset the margin and reputational downsides, then they may start backing away from delivery services. Former Uber CEO Travis Kalanick seems convinced that the solution lies in so-called dark kitchens, where a restaurant operates a food-preparation site at a low-rent location that’s dedicated to deliveries. He has a new startup doing just that, though the approach is not without its problems.

Uber recognizes that losing restaurants is a risk to its business — it said as much in the IPO prospectus. It seems already to be taking steps to prevent it: Uber’s cut fell from 20 percent of gross revenue in 2017 to 18 percent last year.

One ominous antecedent is the experience of Groupon Inc. The Chicago-based website had a simple premise: Restaurants and shops were promised a stampede of customers drawn from its subscriber base, provided they pay a commission and offer steep discounts. It’s not a perfect comparison — food delivery is unlikely to be a fad. But the allure of growth that Groupon presented to eateries, albeit at the expense of profit margins, seems to be similar to the offering from Uber Eats.

In the months after its 2011 IPO, Groupon’s valuation hit $16 billion. Its market capitalization has since slumped to $2 billion as retailers and restaurant owners abandoned its offering, despite a substantial base of 48 million subscribers. Khosrowshahi must be aware of the precedent, but he’s yet to address it publicly.

Though Uber Eats had 15 million customers in the fourth quarter, the signs of strain may already be showing.

Gross bookings hit $7.9 billion in 2018, more than triple the take in the previous year. Khosrowshahi told Forbes the figure would reach $10 billion in 2019. That implies a 26 percent annual increase. Given the firm estimates it has only 1 percent of the global food delivery market, any suggestion of slowing growth should give pause to those perusing its stock offering.

It’s a market with steep competition, too. The company has an edge over most other players, given how well capitalized it is. If it comes down to a price war to retain eateries, drivers and customers, then it is well placed to win.

But ultimately it’s the restaurants who need to know they can make reasonable returns in the long term for their business to be sustainable. Khosrowshahi needs to demonstrate how he can keep both the food industry and his investors happy.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Alex Webb is a Bloomberg Opinion columnist covering Europe’s technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

©2019 Bloomberg L.P.

This article was written by Alex Webb from Bloomberg and was legally licensed through the NewsCred publisher network. Please direct all licensing questions to [email protected].