Skift Take

As restaurants analyze threats to their business they need to work extra hard to see through the hype.

— Jason Clampet

I’m starting to think we’ve hit “peak subscription box.”

You know the drill: You sign up online with the likes of Birchbox, BarkBox, Bulu Box or Bitsbox, and the company sends you a container full of specialized goodies. The format has been embraced by a seemingly unsustainable number of competitors and applied to increasingly obscure niches of merchandise.

And yet we still see plenty of businesses and investors betting this model has shelf life.

Most prominently, Stitch Fix Inc. and Blue Apron Holdings Inc. debuted on the public market this year. JC Penney Co. Inc. announced this month it is partnering with Bombfell.com on a subscription box for big and tall men. Gap Inc. recently launched such a service for its babyGap brand. ThredUp, a fast-growing online secondhand shop, made its foray into the box wars this week with its so-called Goody Boxes, a personalized selection of thrifted apparel.

At this point in the box craze, let me offer some advice — and in true subscription-box style, I will tailor it just for you.

Retailers: Do not join this fray now. Entrepreneurs: Direct your creativity elsewhere. Wall Street and venture capitalists: Apply a heaping dose of skepticism every time you evaluate these businesses.

That’s because subscription boxes, at best, are destined to be a relatively small niche of the booming e-commerce world — and, at worst, could go bust like some buzzy online models of the recent past.

Let’s examine Blue Apron — and for a moment, put aside the fulfillment-center snafus and c-suite musical chairs that have sent its stock on a (mostly downhill) rollercoaster ride. Blue Apron says the addressable market for its business is vast — that it can court a wide variety of customers and grab a piece of spending that might once have gone to either supermarkets or restaurants.

But look at how its business is divided between two-person and four-person plans:

It’s true the family plan hasn’t been around quite as long. But I think this tells us Blue Apron works best for a certain kind of household — one that doesn’t have kids who are picky eaters, for example, or one in which parents don’t spend half their evening ferrying kids to choir practice.

Even in the two-person plan, think about all the constraints there are to using this service regularly: You have to enjoy cooking. You must have a predictable-enough schedule to order food in advance. Your taste in food must be somewhat adventurous.

With each one of those conditions, you likely slash thousands, probably even millions of people from the addressable market.

And that’s just Blue Apron, the U.S. meal-kit market-share leader. Think about what tough going it will be for smaller meal-kit competitors.

Blue Apron is working to expand its pool of potential customers by adding more varied meal plans and emphasizing its lineup of 30-minute dishes, which may help. But the composition of its customer base so far illustrates the challenges all box businesses face in trying to make it big.

Plus, I can’t help but think the box frenzy has something in common with earlier solar flares in e-commerce. Remember LivingSocial and Groupon, and how their fresh approach to deals made them industry darlings for a while? That didn’t last.

Remember when Gilt Groupe was a retailing star, its flash-sale model thought to be an innovation and not a gimmick? It was bought last year by Hudson’s Bay Co. for $250 million, far less than the $1 billion valuation it had in 2011.

Those businesses have something in common with today’s wave of curated boxes. They scored initially because of their novelty, because they brought an element of serendipity to shopping. And then the excitement wore off when the ritual got tiresome and the market got too crowded.

This seems inevitable for many of the box businesses. Once your daughter has done a few kiddie craft projects, how many more is she clamoring for? How often do you really care to experiment with new treats for your dog? Did you ever need a subscription for “Dirt of the Month”?

Plus, as ThredUp CEO James Reinhart pointed out to me this week, subscriptions can be an easy place to cut back if shoppers start to re-evaluate their spending. (That’s one reason why ThredUp is not using a subscription model for its box.)

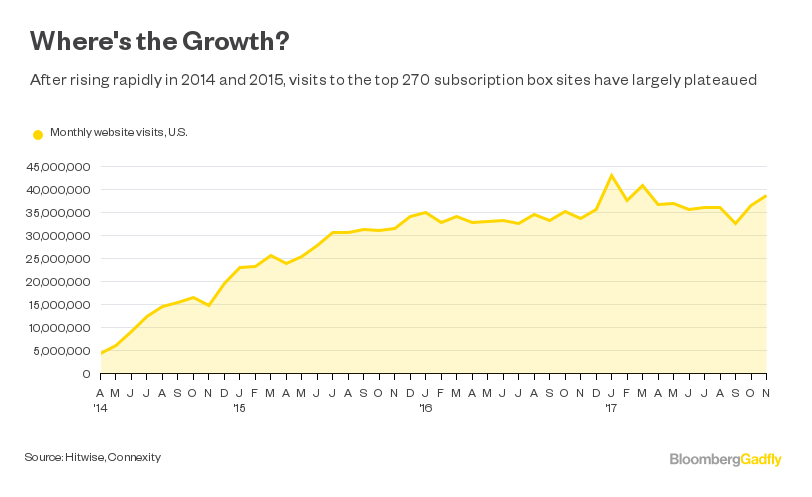

There are hints the biggest days of growth for box businesses are probably behind us.

I don’t necessarily think all of these businesses are destined to fail. As Gadfly’s Shira Ovide has written, Stitch Fix — unlike many Silicon Valley startups — already has the balance sheet of a real business.

I can even imagine a future for Blue Apron where it focuses on courting foodies and cooking enthusiasts with its farm-to-table ethos and unique ingredients, a model that would center on fatter margins and not massively growing its customer base.

But success stories will be the exception, not the rule. And troubled retailers such as Gap and JC Penney should not even bother with a model that can, if anything, only help around the edges.

©2017 Bloomberg L.P.

This article was written by Sarah Halzack from Bloomberg and was legally licensed through the NewsCred publisher network. Please direct all licensing questions to [email protected].

![]()